SUSTAINABILITY

SALM-SALM SUSTAINABILITY CONVERTIBLE

The Salm-Salm Sustainability Convertible Fund invests globally in convertible bonds issued by companies that operate sustainably.

In our investment process, we ensure that convertible bond issuers are examined based on extensive exclusion criteria from a social, governmental and environmental perspective. We mitigate climate risks by actively reducing our carbon footprint. By investing in convertible bonds, we finance the growth of promising and innovative companies in the real economy. Combined with our credit and sustainability analysis, we offer our investors an individually selected, qualitatively convincing sustainability investment in convertible bonds.

Share Classes

Investment process

Economic optimization

The primary factor in the selection process for convertible bonds is bottom-up analysis. The most important factor in the valuation and selection of individual securities is the credit and issuer quality (credit), followed by the equity and conversion potential of the convertible bond, as well as the asymmetric opportunity and risk profile desired for this asset class.

As part of the holistic company valuation, Salm-Salm & Partner performs a comprehensive equity analysis. The equity valuation tool developed by Salm-Salm & Partner is based on a multi-factor model, with the bottom-up analysis having a stronger weighting than the top-down analysis.

In addition to delta - the key figure for stock sensitivity - up to 30 other fundamental decision parameters are applied, including credit rating, stock potential, residual maturity and current interest rate. Technical factors are included in the overall assessment regarding the characteristics of the convertible bond and the option component, as well as the prospectus analysis.

Due to the benchmark-oriented approach to avoid regional and sectoral cluster risks, the analysis focus is on the valuation and selection of individual securities - not on individual regions or sectors.

Credit rating

For investment risk assessment, credit research and in-depth individual security evaluation are of crucial importance. The top priority for Salm-Salm & Partner as a bond investor is the quality of the credit and the associated promise of repayment by the issuer.

To comprehensively measure credit quality, Salm-Salm & Partner first uses official ratings from rating agencies (S&P, Moody's, Fitch). However, due to the occasionally low coverage of official ratings for convertible bonds, Salm-Salm & Partner developed its own proprietary system (VAG compliant) for calculating credit ratings (Asset Manager Rating) at an early stage. Thereby, Salm-Salm & Partner ensures that the credit quality (including balance sheet ratios, credit spreads and business risks) of all relevant issuers is analyzed and evaluated in depth. Any changes in the credit spread or credit spread risks are to be addressed through appropriate single-asset transactions.

Sustainability Criteria

The responsible treatment of humans, nature and the environment is deeply anchored in our beliefs and our understanding of values. In 2012, this set of values was transparently set out for the first time in a sustainable investment process. Since then, we have also been a signatory to the PRI (Principles of Responsible Investment). The sustainability (ESG) concept is enormously complex and has evolved tremendously since the first definitions (Brundtland Report 1987). Thus, we also continuously adapt to new insights, measurement methods and necessities. The path to better sustainability and the active assumption of responsibility beyond the economic factor is our aspiration. From defining initial revenue thresholds, complete exclusions of controversial business practices and models, and a strict best-in-class approach, we have continued to refine our process. In 2016, we took the decisions of the Paris Climate Conference as an opportunity to integrate climate protection into our investment process. We are continuously developing the measurement and reduction of the carbon footprint across all our portfolios. In particular, we are proud to be able to measure the impact of our investments on global warming in degrees Celsius together with the Frankfurt-based company right.based on science. Global warming may be less than two degrees Celsius if all companies operated in the same way as those we allocate.

Climate optimization (footprint)

CO2 footprint Analysis: Since 2017/18, equity and convertible bond research has systematically collected data to determine the CO2 footprint. Since 2019, these are published on the factsheets and the website. In doing so, the CO2 footprints of the respective sustainable mutual funds are set in relation to those of their respective benchmarks.

With this approach, Salm-Salm & Partner essentially pursues three goals:

- The CO2 footprint is determined as a KPI (key performance indicator), which is to be reported on regular and comprehensive basis. The aim is to create the greatest possible publicity. Clients should be able to track the CO2 profile of both funds at any time.

- The CO2 footprint should be significantly lower than that of the respective benchmark in order to convince clients of the advantages of active investment strategies.

- The CO2 footprint should decrease continuously over time until it reaches a level that is no longer reducible or only reducible by applying additional strategies and measures.

Sustainability approach

Classified according to Article 9 SDFR

of the EU Disclosure Regulation

Classified according to Article 9 SDFR

Description of how sustainability risks are included in investment decisions and the result of the assessment of the expected impact of sustainability risks on returns.

As part of its investment process, the company includes all relevant financial risks in its investment decisions and evaluates them on an ongoing basis. In doing so, it also takes into account all relevant sustainability risks within the meaning of Regulation (EU) 2019/2088 of the European Parliament and of the Council of 27 November 2019 on sustainability-related disclosure requirements in the financial services sector ("hereinafter Disclosure Regulation") that may have a material adverse effect on the return of an investment.

Sustainability risk is defined as an environmental, social or governance event or condition, the occurrence of which could have a material adverse effect on the value of the investment. Sustainability risks can therefore lead to a significant deterioration in the financial profile, liquidity, profitability or reputation of the underlying investment. Unless sustainability risks are already taken into account in the investment valuation process, they may have a material adverse effect on the expected/estimated market price and/or liquidity of the investment and thus on the return of the fund. Sustainability risks can have a significant impact on all known risk types and contribute as a factor to the materiality of these risk types.

For more information on how sustainability risks are incorporated into the investment process and the potential magnitude of the impact of sustainability risks on returns, please refer to the respective asset manager's website for outsourced portfolio management mandates. Otherwise, you can find the information on the Universal-Investment website.

Description of environmental and/or social characteristics

Salm-Salm & Partner takes particular account of the aspect of climate protection in connection with the areas of environment, social affairs and corporate governance. In addition to this, Salm-Salm & Partner has developed an individual ESG sustainability rating profile in cooperation with its data providers based on a variety of criteria in line with leading guides in the German-speaking market. The following ESG areas are taken into account:

Environment (turnover thresholds):

- Nuclear energy (0%)

- Fossil energies (0%)

- High volume fracking (0%)

- Oil sands (0%)

- Animal testing (0%)

- Biocides (0%)

- Green genetic engineering (0%)

Social (revenue thresholds):

- Gambling (0%)

- Pornography (0%)

- Spirits/alcohol (10%)

- Tobacco products (0%)

- armaments (0%)

- outlawed weapons (0%)

- embryo research (0%)

Corporate governance (revenue thresholds):

- Exclusion of controversial business practices (corruption, bribery, accounting, tax, competition).

- Norm-based screening (ILO conventions, OECD guidelines for MNCs, UN Global Compact, SIPRI).

CO2 footprint has been collected for the fund for the first time since 2017. In addition, all investments in coal, gas and oil have been excluded since the introduction of the SSP Climate Change Policy. Since 2020, it has additionally been determined which climate impacts, along the Paris climate targets adopted by the United Nations in 2015, emanate from the fund, expressed in degrees Celsius, as a so-called "forward-looking" climate metric. If all companies were to operate in the same way as those allocated in the portfolio, global warming would be less than 2 degrees Celsius, according to the evaluation by right. based on science as of Feb. 16, 2021.

Do companies in which investments are made apply good corporate governance practices?

Directive 2013/34/EU of the European Parliament and of the Council sets out transparency obligations with regard to environmental, social and corporate governance aspects in the context of non-financial reporting. The fund invests exclusively in companies that demonstrate good corporate governance practices. Companies are expected to publish a corporate governance code in accordance with national legislation, in which they demonstrate at least sound management structures, a proper relationship with employees, employee compensation and tax compliance.

In order to assess good corporate governance, priority is first given to a so-called "best-in-class" analysis. Here, weightings of the top levels of ESG company ratings as well as industry-specific minimum ratings are defined as a threshold that may not be fallen short of.

Methods for assessing, measuring and monitoring environmental and/or social characteristics.

Salm-Salm & Partner works with a variety of research houses, including well-known market giants such as MSCI ESG and start-ups such as the Frankfurt-based Fintech right. based on science. Other external sources include Altert services from providers such as Bloomberg, Google and the Sustainable Business Institute (SBI).

In addition, the expansion of complementary, predominantly qualitative in-house analyses is being pushed. Currently, two analysts are collecting additional information, mainly based on publicly available platforms and information services (including Science Based Targets, Clean 200, Carbon Underground, Influence Map). Much of this internal analysis is based on climate-related data.

The ESG evaluation and rating system is an integral part of Salm-Salm & Partner's investment process.

The central criterion for the selection of individual securities is the credit quality of the companies. Due to the large number of non-rated credit ratings in the asset class of convertible bonds, Salm-Salm & Partner developed its own credit rating system at an early stage. This is classified by the capital management company Universal-Investment- Luxemburg S.A., as compliant with the Insurance Supervision Act (VAG).

In this way, Salm-Salm & Partner ensures that the credit quality (including balance sheet ratios, credit spreads and business risks) of all issuers that qualify for investment is analyzed and evaluated in depth. As part of the holistic company valuation, Salm-Salm & Partner performs a comprehensive equity analysis.

The sustainability analysis follows the evaluation of market capitalization, credit rating and volatility of relevant stocks and runs parallel to the evaluation of the companies' business models, balance sheet, capital structure as well as regional and sectoral distribution.

First, all companies are subjected to an exclusion screening in various business areas and practices. In the following step, a sustainability rating, the so-called "ESG Performance Score" is assigned.

For the further selection process, Salm-Salm & Partner only uses stocks that withstand the analyses and exclusion criteria and whose issuers can demonstrate an ESG Performance Score of at least 4. The scale ranges from 0 to 10.

Negative screening is based on the MSCI ESG online platform, while the evaluation of positive criteria is primarily based on the best-in-class rating system developed specifically for Salm-Salm & Partner.

The absolute best-in-class approach is based on the fact that the environmental and social challenges in the individual sectors as well as for companies and countries are very different.

Awarded with the FNG seal

Awarded the FNG seal every year since 2016, and with two stars since 2019

Awarded with the FNG seal

The FNG seal for sustainable investment funds was developed by the Forum Nachhaltige Geldanalgen (FNG) together with financial experts and civil society actors in a three-year exchange. One of the core tasks of the FNG is to further develop and continuously improve quality standards for sustainable investment products in order to ensure the quality of sustainable investments. The seal concept itself is also constantly being developed further together with an independent committee and thus adapted to the dynamics of the sustainable investment market as well as to new requirements.

The FNG seal at a glance:

- Quality assurance of sustainable investments

- Minimum requirements according to internationally recognized standards

- Reduced time and costs for investors and fund providers

- Verification by an independent auditor

- Promotion of the sustainable investment market

Our Salm Sustainability Convertible has been awarded the FNG seal every year since 2016, and two stars since 2019

The FNG seal is awarded annually. For more information, please click here.

Compatible with Finanko criteria

the Austrian Bishops' Conference and the Religious Communities of Austria

Compatible with Finanko criteria

The responsible handling of money is a self-evident obligation from the Gospel for the mission and credibility of the Catholic Church. An expression of this is the "Guideline on Ethical Investments" (FinAnKo) adopted by the Austrian Bishops' Conference in 2017.

"Guidelines for Ethical Investments" (FinAnKo). The criteria contained therein follow the proven triad of ecumenical-Christian ethics and are justice, peace and integrity of creation. This regulation is continuously reviewed and, if necessary, further developed.

Most recently, in 2019, a full phase-out was decreed for church investments in those companies that extract or produce fossil fuels (coal, oil, natural gas). The Austrian Bishops' Conference has signed a corresponding divestment declaration within the framework of the Global Catholic Climate Movement (GCCM) and adapted its ethical investment guidelines accordingly.

Zuletzt wurde 2019 bei kirchlichen Veranlagungen ein Vollausstieg in jenen Unternehmen verfügt, die fossile Brennstoffe (Kohle, Öl, Erdgas) fördern bzw. produzieren. Die Österreichische Bischofskonferenz hat eine entsprechende Divestment-Erklärung im Rahmen des "Global Catholic Climate Movement" (GCCM) unterzeichnet und ihre ethischen Veranlagungsrichtlinien entsprechend angepasst.

MSCI ESG

With over 40 years of experience in sustainability analysis, a strong partner for our research process.

MSCI ESG

MSCI has over 40 years of experience in sustainability analysis. The company collects ESG data from thousands of sources, cleansing, standardizing and modeling it to create a precision tool for discovering true ESG performance.

Integrating MSCI ESG ratings into the investment decision-making process helps identify risks or opportunities that may not be captured by traditional financial analysis - incorporating these issues helps minimize risk and increase long-term returns.

More

Best in Class

Our approach is to invest in the companies that are leading the way and implementing sustainable aspects in an exemplary manner.

Best in Class

The Salm Best-in-Class approach ensures that investments are made exclusively in the upper median of all companies that we have analyzed according to sustainability aspects.

In addition, we conduct intensive CO2 research to ensure that the fund's carbon footprint is significantly below the benchmark and complies with the goals of the Paris Climate Conference. For this purpose, we work together with the analysis company Right. based on science. The climate model evaluates the climate strategy of the analyzed companies in the portfolio for the future.

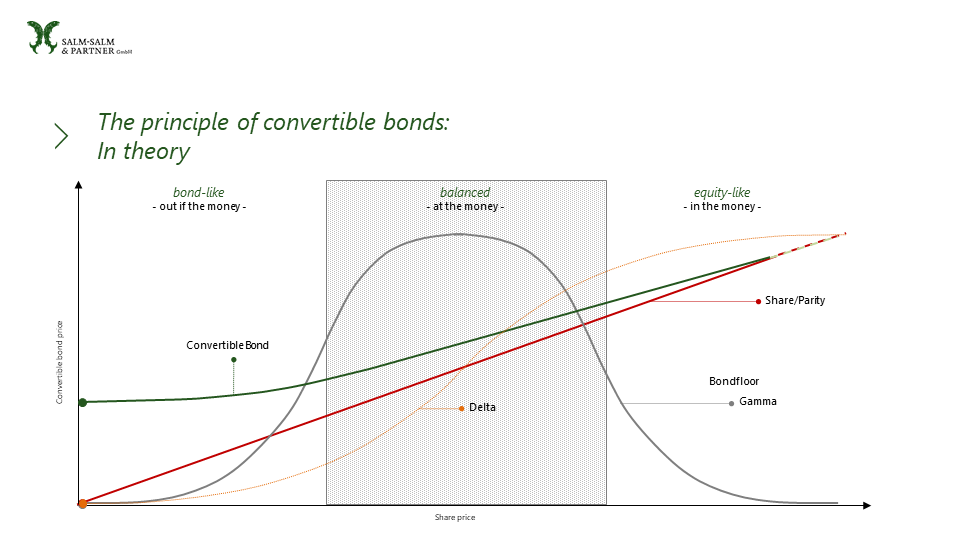

In theory

The principle of the convertible bond

A convertible bond can assume three aggregate states: balanced, equity-like and bond-like.

Convertible bonds are usually in the balanced range at the time they are issued. Increases in the share price have a greater effect on the price of the convertible bond than decreases.

If the share price continues to rise, a convertible bond evolves to become more equity like. It reacts stronger to changes in the share price.

The third status - bond-like - describes a convertible bond whose underlying equity has declined to such an extent that the exercise of the call option is unlikely. Changes in the share price have only a minor effect on the price of the convertible bond. The bond-like convertible bond behaves like a conventional bond of the issuer.

Are you a private or institutional investor?

Salm-Salm & Partner supports its investors with a broad range of information on asset allocation, investment management and market information. It is therefore important for us to know what type of investor you are. Professional investors according to §67 WpHG are institutional investors and distributors. To help us provide you with the right information, please select one of the following options. Translated with www.DeepL.com/Translator (free version)

Salm-Salm & Partner accepts no liability for the unauthorised use of the following content.